MVA

You were in a collision somewhere around Thornhill — maybe on Yonge, maybe merging onto the 407, maybe a fender-bender in a plaza lot off Centre Street. You reported it, you started care, and your provider sent your insurer a treatment plan. Then a letter arrives saying it's been denied or only partly approved.

It feels personal. It usually isn't. In Ontario, your treatment plan is a funding request submitted on a form called the OCF-18 (Treatment and Assessment Plan), and the insurer is required to respond to it. A denial is the start of a process, not the end of your care — and understanding why it happened is the first step to getting the decision reversed.

This page explains, in plain terms, how treatment approval works under Ontario's no-fault system, the real reasons plans get denied, and what your options are.

Every auto policy in Ontario includes Statutory Accident Benefits (SABS) — coverage for medical and rehabilitation care after a collision, regardless of who caused it. It applies whether you were the driver, a passenger, a cyclist, or a pedestrian, and it's separate from OHIP and from your workplace benefits.

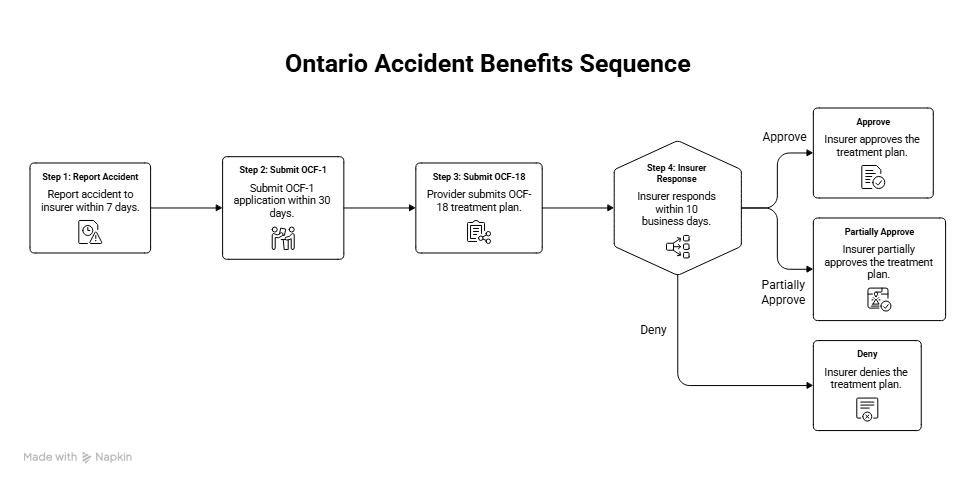

Here's the sequence most people in York Region go through:

One detail worth knowing: if the insurer doesn't respond within 10 business days, they become liable to pay for the proposed treatment provided from the 11th day onward, until they do respond. Silence is not the same as denial.

**Did You Know?**Treatment within the first five days after a collision does not require pre-approval. Ontario's rules let you start emergency and early care right away — you don't have to wait on a form to begin getting help.

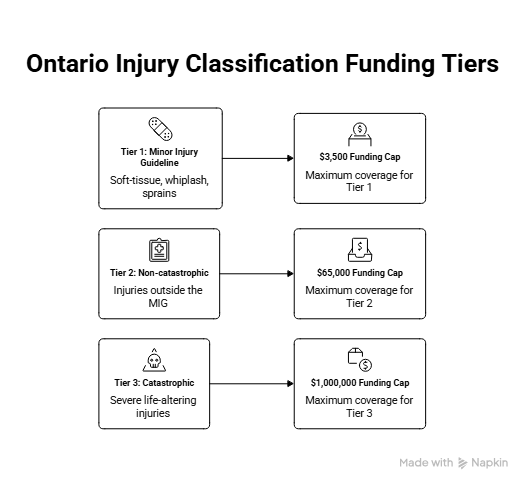

The amount of treatment funding available depends on how your injuries are categorized. This classification is often the real story behind a denial.

Minor Injury Guideline (MIG) — Soft-tissue injuries such as sprains, strains, whiplash-associated disorders, contusions, and abrasions are typically capped at $3,500 in total medical and rehabilitation benefits. Care under the MIG can begin without pre-approval once an OCF-23 (Treatment Confirmation Form) is completed.

Non-catastrophic (outside the MIG) — Injuries that fall outside the MIG definition open up coverage of up to $65,000 for combined medical, rehabilitation, and attendant care (unless optional benefits were purchased).

Catastrophic — The most severe, life-altering injuries access a combined limit of up to $1,000,000.

A very common scenario: your insurer holds your injuries inside the MIG and its $3,500 cap, while your clinician believes your injuries are more significant. When your provider submits an OCF-18 to fund care beyond that cap, the insurer denies it — because, from their file, you're still "minor." The disagreement isn't really about one treatment plan. It's about which box your injuries belong in.

**Did You Know?**Psychological injuries can be removed from the Minor Injury Guideline. If accident-related symptoms — for example, a diagnosed phobia, PTSD, or a major depressive episode — go beyond what's considered "minor," your clinician can submit compelling evidence to move you out of the MIG and unlock significantly more coverage.

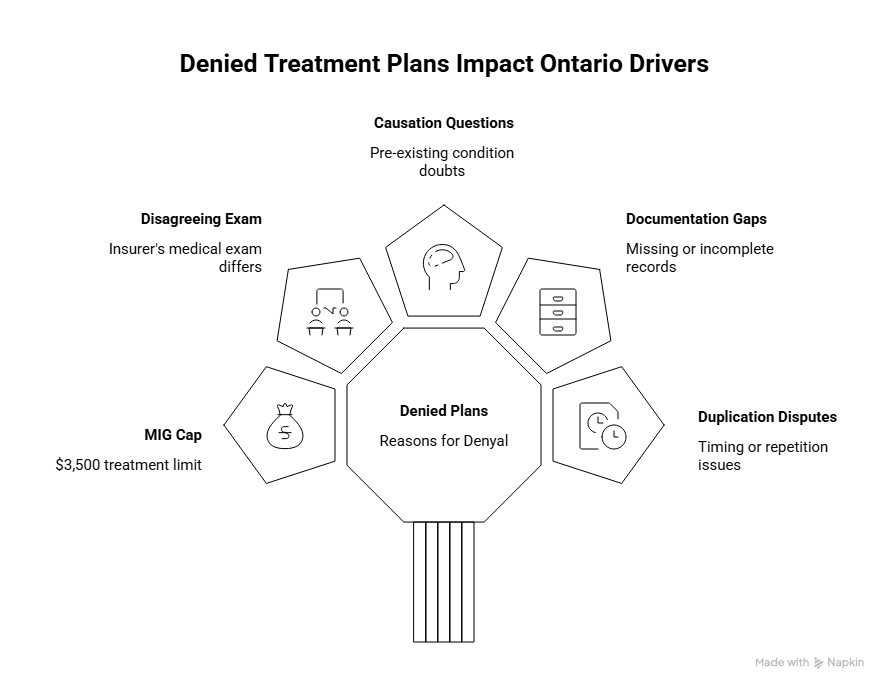

Denials rarely arrive with a detailed explanation. Often it's a short letter stating the proposed care is "not reasonable and necessary," or outside the scope of the claim. Behind that phrase, the common drivers are:

1. MIG classification. Your insurer is keeping you inside the $3,500 minor-injury cap, so any plan asking for more is refused.

2. Insurer's medical assessment disagrees. The insurer arranges its own examination (an Insurer's Examination, sometimes called an IME). If that assessor's opinion differs from your treating clinician's, the plan can be denied on the strength of the insurer's report.

3. Causation questions. The insurer argues your symptoms aren't connected to the collision — pointing to a pre-existing condition or a gap in your records. Important: a pre-existing condition does not automatically disqualify you. The record simply needs to explain your pre-accident baseline and how the collision changed it.

4. Documentation gaps. Inconsistent clinical notes, unclear functional limitations, or a weak link between the proposed care and accident-related impairments. Errors and missing information on OCF forms are among the leading causes of delayed and denied claims.

5. Duplication or timing. The insurer believes the care overlaps with something already approved, or disputes when and how much treatment is appropriate.

The throughline: most denials are a documentation and evidence problem, not a verdict on whether you're actually injured.

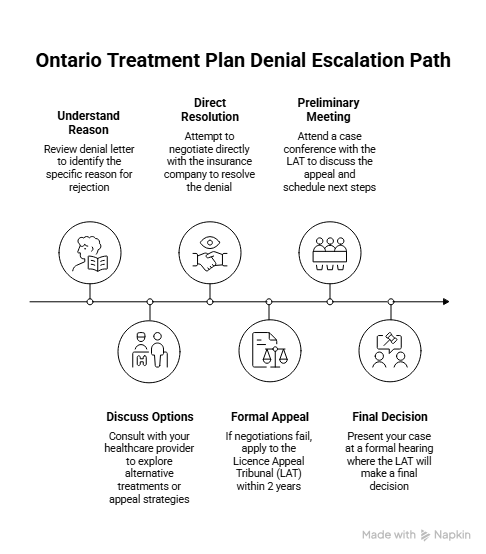

A denial is appealable, and many are overturned once the record is clarified. Your options, in rough order:

Read the denial letter closely. By law, the insurer must put the reason for the denial in writing every time it makes a decision affecting a benefit. That stated reason tells you exactly what to address.

Talk to your provider. A clinic experienced with MVA claims can respond to the specific reason — sharpening the OCF-18 rationale, adding functional measures, documenting your baseline, or supporting a request to be removed from the MIG.

Negotiate first. Before any formal dispute, exchanging documents (like a hospital discharge summary) and attempting to resolve the disagreement directly with the insurer is encouraged and sometimes resolves it.

Apply to the Licence Appeal Tribunal (LAT). If it can't be resolved, disputes go to the LAT – Automobile Accident Benefits Service (LAT-AABS), the body that now handles SABS disputes in Ontario. Key facts:

You're allowed to represent yourself, but because LAT decisions lean heavily on medical records and well-prepared submissions, many people work with a personal injury lawyer at this stage.

**Did You Know?**Some people continue necessary treatment privately while a dispute is underway and seek reimbursement later, if their provider and budget allow. Whether that's wise depends entirely on your situation — it's a conversation to have with your clinician.

Treatment plans in York Region are reviewed by the same major carriers that dominate Ontario's market. You'll recognize most of them from your pink slip:

Every one of these insurers follows the same SABS rules and the same OCF-18 process described above. The form, the 10-business-day response window, the MIG cap, and your two-year LAT timeline don't change based on which company's name is on your policy.

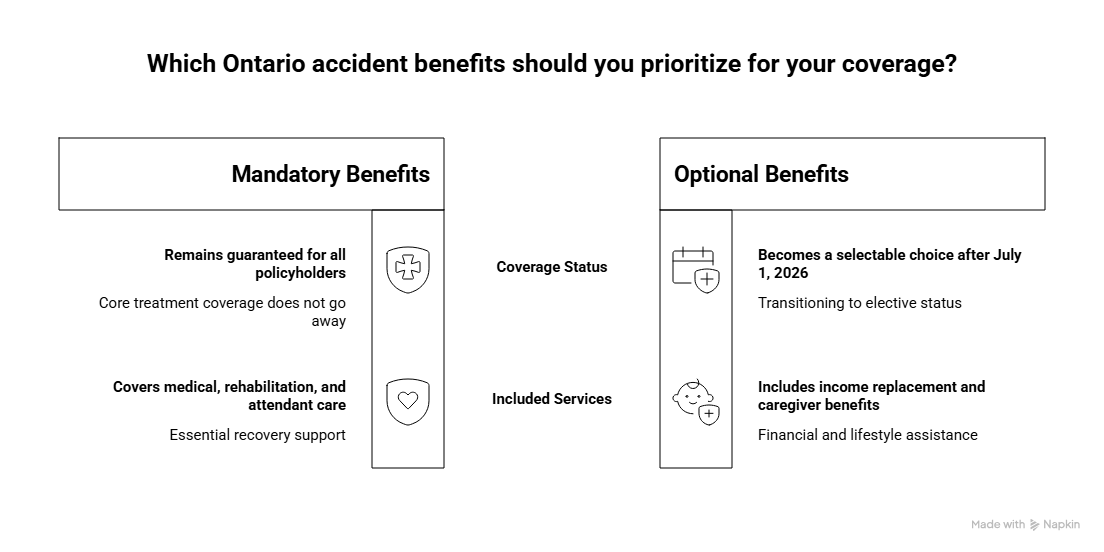

Ontario's accident benefits system is being restructured. As of July 1, 2026, for policies issued or renewed on or after that date, several accident benefits — such as income replacement and caregiver benefits — become optional rather than automatic. Drivers will need to actively choose those coverages when buying or renewing.

The key takeaway for treatment: medical, rehabilitation, and attendant care benefits remain mandatory in every Ontario auto policy. Your core coverage for physiotherapy, chiropractic, and rehabilitation care after a collision is not going away. But it's worth reviewing your policy at renewal so you understand exactly what you've opted into.

A denial letter is most discouraging when you're already in pain and trying to recover. The practical reality is that the quality of your documentation and your care team's familiarity with the SABS process directly affect how your claim moves. A provider who understands OCF-18 submissions, MIG classifications, and what insurers expect can keep your file clear, complete, and harder to deny.

If your treatment plan was denied or only partly approved after a motor vehicle accident, our team in Thornhill can review where your claim stands, treat your accident-related injuries, and make sure your documentation reflects what you're actually dealing with.

This page is general information about Ontario's accident benefits system and is not legal advice. Coverage, deadlines, and outcomes depend on your individual policy and circumstances. For advice specific to your claim, speak with a licensed Ontario personal injury lawyer.

This page is general information about Ontario's accident benefits system and is not legal advice. Coverage, deadlines, and outcomes depend on your individual policy and circumstances. For advice specific to your claim, speak with a licensed Ontario personal injury lawyer.

Recover faster, move better, and feel stronger with expert physiotherapy. Our team is here to guide you every step of the way.

.webp)

.webp)

.webp)